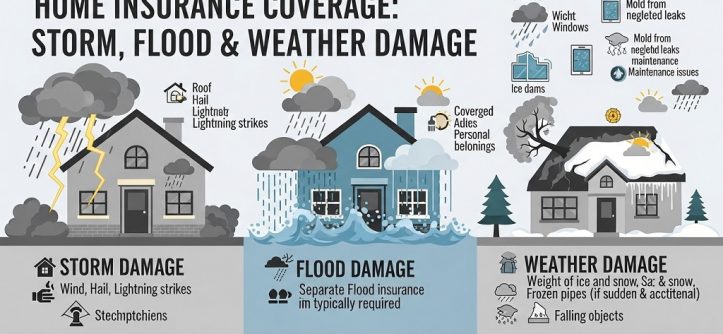

Most home insurance policies cover damage caused by storms such as wind, hail, lightning, and fallen trees but they usually do NOT cover flood damage unless you purchase separate flood insurance.

Why understanding weather damage coverage matters more than ever

Home insurance typically protects against windstorms, hail, lightning strikes, and storm-related structural damage—but excludes flooding from external water sources unless a dedicated flood insurance policy is added. Many homeowners only discover this gap after severe weather causes expensive losses.

Extreme weather events are increasing worldwide. According to global insurance industry reports, weather-related disasters account for the majority of residential property claims every year. Yet many homeowners assume all storm damage is automatically covered. That assumption can lead to denied claims and unexpected repair costs.

If a roof collapses after a cyclone, coverage usually applies. If rainwater enters through a broken window during a storm, coverage often applies. But if rising floodwater damages the same house, the claim is commonly rejected without a flood endorsement.

This article explains exactly how home insurance handles storm, flood, and weather damage. You’ll learn what is covered, what is excluded, how policies differ, and how to avoid costly surprises before the next severe weather event.

Does home insurance cover storm damage?

Yes. Standard home insurance policies usually cover storm damage caused by wind, hail, lightning, and falling debris, provided the damage is sudden and accidental.

Storm damage coverage typically applies to both the structure of the home and personal belongings inside. Coverage depends on the policy type and insurer terms, but most policies protect against:

- Windstorm damage to roofs and walls

- Broken windows from flying debris

- Lightning-related fires

- Hail damage to siding and shingles

- Fallen trees damaging the structure

For example, if strong winds tear shingles off your roof during a storm, your insurer will generally pay for repairs after deductibles are applied.

However, insurers may deny claims if maintenance issues contributed to the damage. A weakened roof that collapses due to neglect may not qualify for coverage.

Does home insurance cover wind damage inside the house?

Yes. Interior damage caused by wind entering through storm-created openings is usually covered under standard policies.

If wind breaks a window and rain damages furniture, both structural repairs and contents replacement are typically included in the claim.

Does home insurance cover flood damage?

No. Standard home insurance policies almost never cover flood damage caused by rising water from rivers, heavy rain accumulation, or storm surges.

This is one of the most misunderstood areas of home insurance coverage. Flood damage refers to external water entering a home from ground level upward.

Examples of excluded flood events include:

- Overflowing rivers

- Storm surge from coastal storms

- Flash flooding after heavy rainfall

- Urban drainage overflow

- Surface water entering through doors

To protect against these risks, homeowners must purchase a separate flood insurance policy. In many countries, flood coverage is offered through government-backed insurance programs or private insurers.

Is rain damage considered flood damage?

No. Rain entering through a storm-damaged roof is usually covered, while rainwater rising from outside the home is classified as flood damage and excluded.

The direction of water entry determines coverage eligibility.

What types of weather damage are usually covered by home insurance?

Home insurance generally covers weather-related damage caused by windstorms, hail, lightning strikes, snow weight, and fallen objects resulting from storms.

Covered weather-related risks typically include:

- Roof damage from high winds

- Ice dam-related structural damage

- Lightning-caused electrical fires

- Hail dents on exterior surfaces

- Tree impact damage during storms

- Snow load collapse in severe winter regions

Coverage applies when the damage is sudden, accidental, and unavoidable.

Does insurance cover damage from falling trees during storms?

Yes. If a storm causes a tree to fall on your home, repairs to the structure are usually covered.

Tree removal costs may also be partially reimbursed depending on policy limits.

What weather-related damage is NOT covered by home insurance?

Home insurance does not cover flood damage, earthquakes, gradual wear and tear, mold from long-term moisture exposure, or maintenance-related deterioration.

Common exclusions include:

- Flooding from natural water sources

- Ground movement and earthquakes

- Damage from neglected repairs

- Seepage through foundation cracks

- Long-term roof deterioration

Understanding exclusions is critical because insurers evaluate whether damage resulted from a sudden event or long-term conditions.

Does home insurance cover water leaks after storms?

Yes, but only if the leak results directly from storm-related structural damage rather than pre-existing maintenance issues.

How does flood insurance differ from home insurance coverage?

Flood insurance specifically covers rising water damage, while home insurance protects against wind-driven storm damage and structural impacts.

| Coverage Type | Home Insurance | Flood Insurance |

|---|---|---|

| Wind damage | Covered | Not covered |

| Lightning damage | Covered | Not covered |

| Storm surge flooding | Not covered | Covered |

| River overflow | Not covered | Covered |

| Heavy rainfall accumulation | Not covered | Covered |

| Fallen tree damage | Covered | Not covered |

Both policies work together to provide complete weather protection.

Does home insurance cover hurricane or cyclone damage?

Yes. Home insurance usually covers hurricane or cyclone wind damage but excludes storm surge flooding unless flood insurance is purchased.

Wind-related hurricane losses typically covered include:

- Roof removal

- Window breakage

- Exterior siding damage

- Structural collapse from debris

Storm surge water entering homes remains excluded without flood coverage.

Are hurricane deductibles different from normal deductibles?

Yes. Many insurers apply separate percentage-based deductibles for named storms, which can increase out-of-pocket costs significantly.

Does home insurance cover lightning strike damage?

Yes. Lightning-related fire and electrical damage are covered under most standard home insurance policies.

Coverage typically includes:

- Electrical wiring repairs

- Appliance replacement

- Fire restoration costs

- Structural damage repairs

Lightning claims are among the most common severe weather insurance claims globally.

Does home insurance cover roof damage from storms?

Yes. Storm-related roof damage is covered when caused by wind, hail, or falling debris rather than aging or poor maintenance.

Insurance companies assess roof condition before approving claims. Older roofs may receive partial reimbursement depending on depreciation.

Will insurance replace an entire roof after storm damage?

Sometimes. Full replacement is approved when damage affects structural integrity across large areas of the roof.

Minor damage typically results in partial repair coverage instead.

Does home insurance cover basement water damage from storms?

Sometimes. Coverage applies if water enters through storm-damaged structures but not if flooding rises from outside ground level.

Basement protection may require optional add-ons such as:

- Sewer backup coverage

- Drain overflow protection

- Sump pump failure endorsement

These endorsements significantly expand protection against heavy rainfall events.

How can homeowners strengthen coverage against severe weather risks?

Homeowners can improve protection by adding flood insurance, increasing dwelling limits, and purchasing endorsements for sewer backup and water intrusion risks.

Practical steps include:

- Review policy exclusions annually

- Add flood coverage if living in risk-prone areas

- Upgrade roof materials

- Install storm shutters

- Maintain drainage systems

- Document home condition with photos

Risk mitigation often lowers insurance premiums as well.

Conclusion: How to make sure your home is fully protected from weather damage

Home insurance provides strong protection against windstorms, lightning, hail, and falling debris—but it does not cover flooding from external water sources. Understanding this distinction is essential for avoiding denied claims and unexpected repair costs after severe weather.

The most effective strategy is combining standard home insurance with targeted endorsements and separate flood insurance coverage where needed. Reviewing your policy annually ensures protection keeps pace with changing climate risks and property conditions.

If you haven’t checked your weather coverage recently, now is the time. A short policy review today can prevent major financial stress after the next storm.

Frequently Asked Questions About Home Insurance and Weather Damage

Does home insurance cover heavy rain damage?

Yes. Heavy rain damage is covered if water enters through storm-created openings, but not if flooding rises from ground level.

Is storm surge covered by home insurance?

No. Storm surge is classified as flooding and requires separate flood insurance coverage.

Does insurance cover snow damage to roofs?

Yes. Damage caused by excessive snow weight is typically covered when structural collapse occurs suddenly.

Are fallen fences covered after storms?

Yes. Detached structures like fences are usually covered under other-structures coverage within home insurance policies.

Does insurance pay for spoiled food after power outages from storms?

Often yes. Many policies include limited reimbursement for food spoilage caused by storm-related electrical outages.

Can insurers deny claims after severe weather events?

Yes. Claims may be denied if damage results from maintenance neglect, excluded flooding, or pre-existing structural issues.

Read More Also: How to Pick the Best Vacuum for Carpeted Stairs Without Overspending

Leave a Reply

Cancel reply